Understanding the small business landscape during the pandemic

How should we think about the different types of small business during the pandemic?

It’s hard to comprehend that our once-busy high streets and town squares now sit largely dormant. But only six months ago it was hard to imagine a government shutting down large sections of the economy and instructing people to stay at home. Although lockdown and social distancing have opened new opportunities for some businesses, many more are facing a struggle for survival. And for those facing that struggle, it’s difficult to see the way forward.

The first challenge is that the ground is constantly shifting. Our understanding of Covid-19 and how it is transmitted is constantly developing, and guidance from public bodies changes frequently. As regulations start to relax, there is still the looming threat of a ‘second peak’. This makes it very difficult for individuals or businesses to plan more than a few weeks ahead, or to think in detail about what a ‘new normal’ might look like for them. For a pub landlord, one metre of social distancing could mean a viable business, with two metres leading to insolvency.

Second, there is little historical precedent to rely on. Businesses have had to overcome a number of economic shocks in the recent past, including the Great Recession (2007–09) and European Debt Crisis (2009–12), but the current crisis is rather different. The contraction of most economies has been far deeper and sharper than previous recessions, and has been triggered by a suppression of supply, and mass shifts in demand to new channels, rather than a simple collapse in demand itself. No one can be sure what the recovery will look like, how effective the government’s response will be, or what the unintended side-effects might be. The strategies that have helped businesses to survive past disruptions may be effective once again, but at the time of writing it is hard to tell.

Thirdly, much of the freely-available advice is well-intentioned, but lacks nuance and tends to treat all small businesses as if they were the same: examples of this can be found in everything from the Harvard Business School Covid-19 center through to Forbes and Entrepreneur.com. There is such diversity in the needs that small businesses serve that we believe it’s impossible to address them as one homogenous ‘sector’. Generic advice may be a helpful starting point, but it won’t be enough for most businesses.

One thing we do believe though, is that small businesses are resilient and they are adaptable given the right understanding of their environment.

Understanding demand

In this changing and unmapped environment, we think it’s helpful to keep things as simple as possible.

For many small businesses survival will depend, in part, on access to low-cost, flexible financing, a sympathetic approach to property and equipment leases, and an accommodating taxation policy. But this isn’t where our main expertise lies. Instead, we will focus on a second vital factor — rebuilding consumer demand. As we described in our first article we’re interested in the contribution that small businesses make to our communities and society, as well as the economy, so we’ll be focusing on B2C businesses that operate primarily from a physical location(s).

Even under ‘normal’ circumstances demand is influenced by a range of factors — including price, benefits and tastes, availability of close substitutes, expected changes in the product or the price in the future, and levels of disposable income. The strength of each of these factors, and how they interact, will vary greatly across different goods and business sectors.

Of course, these rules of demand will still apply in the Covid and post-Covid worlds. Levels of disposable income and personal debt in particular will have a strong bearing on how quickly business recovers, and the compound index that measures these factors has dropped by 9% over the last 3 months alone according to a recent survey by Deloitte. However, governmental and societal responses to the pandemic have added further complexity to the equation.

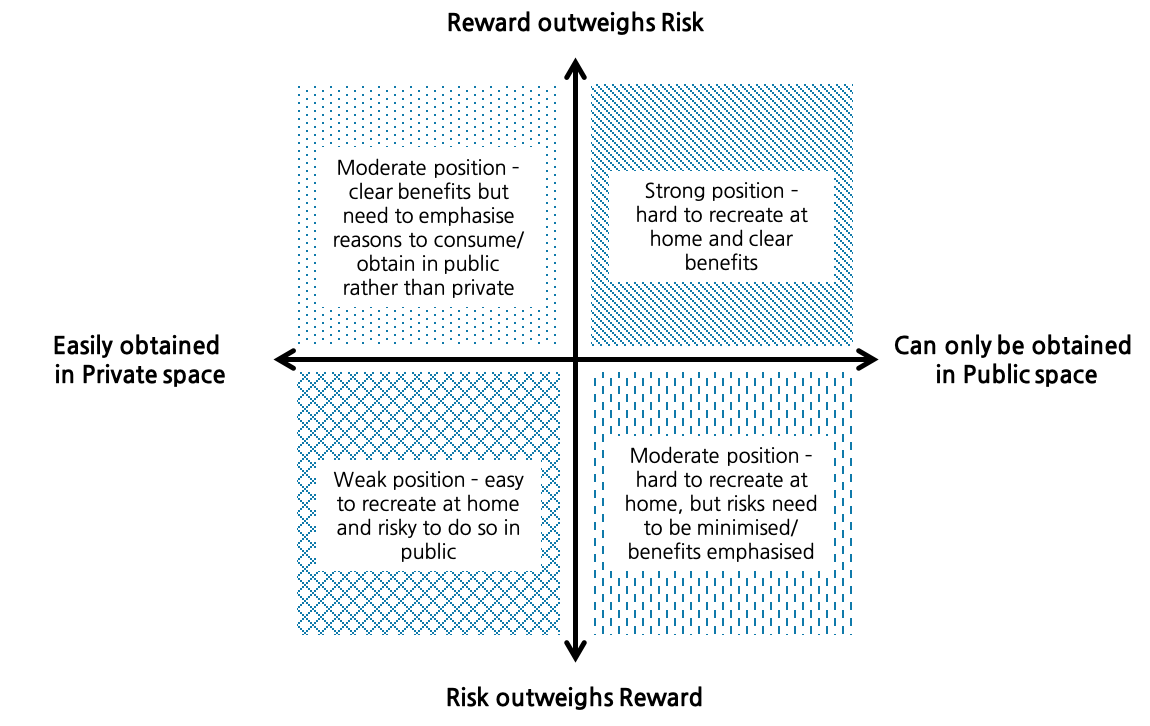

We see two primary forces influencing demand for the goods and services provided by small businesses. We can map small businesses against these two dimensions to understand what the future might hold, and what they can do about it:

Risk vs Reward — does the perceived risk of visiting a physical business now outweigh the benefit gained by doing so?

Public vs Private — is it possible, or even preferable, to obtain a product or gain an experience in a private rather than public space?

Risk vs Reward

The pandemic has introduced a new dimension to consumer decision-making; now the very act of visiting a physical business is perceived as a risk. But, this has to be balanced against the rewards we gain from visiting such businesses.

We define ‘Reward’ as the need (does the business provide goods or services that I see as essential?) and desire (does it provide goods or services that have a high emotional value, or that I feel very attached to?). E.g. a pharmacy that can fulfil prescriptions provides an essential service that is ‘needed’, while a much-loved coffee shop at the heart of a community has a highly ‘desired’ emotional value.

‘Risk’ is made up of the perceived exposure to Coronavirus (how many people do I think I will come into close contact with if I visit this business? Is it a clean environment?) and duration of visit (how long do I spend in that business to gain the benefits I am looking for?). E.g. I might consider visiting a restaurant for a few hours to be more of a risk than popping into a convenience store with a quick check-out lane for one or two items.

Public vs Private

The shift from purchasing and consuming in public to private spaces began long before the Covid pandemic. Delivery services like Ocado, Amazon and Deliveroo have become an easy alternative to visiting a supermarket, department store or restaurant. However, lockdown has certainly accelerated this shift. In the initial stages of the pandemic there was little choice — only “essential” shops remained open — but even as physical business reopen, many consumers may stick with their new-found habits. We have considered two elements which influence whether demand will remain in private or revert back to public spaces: product and experience.

‘Product’ covers whether I can get the items I want delivered to my home. It’s easy to believe that home delivery will replace the weekly supermarket trip for many, but there are still a large range of products that aren’t fully available online — especially those that are tailored or personalised for a specific consumer. And products that require skill to produce are harder to replicate at home. Speaking from experience, I can have ingredients delivered to me by the same wholesaler who used to supply my favourite neighbourhood restaurant, but I certainly can’t replace the skill and technique of their chefs.

‘Experience’ covers whether I recreate the atmosphere (and service) I used to enjoy in public in my home. Whilst it may be easy to receive products at home, it is much harder to recreate experiences. The beer in my fridge may taste just as good as the pint I would be served in the pub, but I can’t mimic the warm, convivial atmosphere in my living room (no matter how many people are joining me on Zoom). Social distancing rules will also influence this balance of public vs. private experience: restaurants, cinemas, gyms and cafes will reopen, but if the queue for entry snakes around the block, and we have to awkwardly maintain a 2m gap to other customers once we’re inside, how pleasurable will that experience be? Would I be better off staying at home?

These two dimensions, Risk vs Reward and Public vs Private can be combined to form a simple chart. Where each business sits on these axes will tell us more about the scale of the challenge they face, and what their strategies might be.

Where do different business types fit?

We have placed a range of business types across these two dimensions to understand what the coming months might look like (compared to pre-Covid demand), and how they might respond. We have tried to make our analysis as rigorous as possible, but it is based mostly on our own observations and intuition. You may have your own interpretation as to where different business types fit across the quadrants, but we think the framework holds true.

Using our model we can divide businesses into four main groups:

Public necessities: Opticians & dentists, hairdressers, pharmacists & chemists.

It is difficult to access the services provided by these businesses at home and there is a clear benefit to visiting them. The risk will be perceived to be relatively low given that there is typically a low number of people in these stores at any given time. Good hygiene has always been important for these businesses, so consumers should have confidence. Demand should rebound quickly, and there is likely to be a strong spike of pent-up demand as soon as they reopenCommunity builders: Coffee shops, café & delis, pubs, bars, restaurants, gyms.

Whilst it may be possible to receive the products these businesses provide at home, it is far more difficult to recreate the atmosphere and experience, and many people have a strong emotional attachment to their local pub or restaurant. However, some will be very nervous about going back to such communal establishments, and strict social distancing, if enforced, will likely diminish the experience for some time.Nice-to-haves: Bookshops, florists, butchers & bakeries, greengrocers, florists.

Dwell-time in these businesses tends to be quite short, which mitigates some of the risk for customers. It is also relatively easy for these businesses to control the number of people in the shop and maintain social distancing. Shopping in these establishments can also be a pleasurable and rewarding experience for the customer. The real threat for these businesses comes from online competition — many consumers have now realised that they can get high-quality fresh produce delivered directly to their home, and have paid longer-term subscription fees to do so.On-the-edge: Newsagents, stationers, convenience stores, DIY & hardware stores. Businesses in this group may have a more transactional relationship with their customers. Although a quick trip to the corner store may be seen as low risk, the perceived reward is also relatively low. The products sold in the businesses are mostly readily available online, which will likely affect their long-term success too — e.g. newspapers can be easily substituted through online copies.

Next week we’ll be working from these four segments to map what recovery could likely look like for each. We’ll also consider the strategies each can adopt to survive, as well as interviewing some business owners to get their views of the challenges they face.

We’d love to hear your thoughts — do you agree with our groupings, or have a different interpretation?

Want to get in touch?

Leave a comment below

Shoot us an email at: theskylarkeditors@gmail.com

Follow us to get updates on articles we write: Follow Rich & Ben

or…!